In 2024, broad trends in investment strategy are changing.

Mixing traditional assets like stocks and bonds with private assets like private equity and private credit is becoming a much more fundamental approach.

Here’s a direct look at each trend, with practical examples.

Shifting Gears in Portfolio Allocation

Investors are moving from the traditional 60/40 stock/bond allocation to a 40/30/30 model, introducing 30% alternative assets into their mix.

This move is likely a response to the fact that 2022 was one of the worst years on record for the traditional 60/40 portfolio split.

The long-trusted 60/40 allocation returned -18.1% in 2022, which is the second worst year on record since the inception of the Bloomberg US Aggregate Bond index.

KKR found that the 40/30/30 portfolio outperformed a traditional 60/40 split by 2.6% over the 24-month period through June.

JPMorgan Asset Management’s analysis showed that reallocating a 60/40 portfolio to 40/30/30 stocks/bonds/alts improved its Sharpe ratio to 0.75 from 0.55 from 1989 to the present.

Alternative Investments Becoming Mainstream

Remember when cryptocurrency seemed like a wild west? Not anymore. With major brokers partnering up with crypto exchanges, digital assets are becoming a staple in many portfolios.

A lot of investors feel way more comfortable buying into Bitcoin or Ethereum now that their trusted brokerages provide a direct, secure gateway.

The development and integration of blockchain into fintech is breaking down a lot of walls around accessibility.

Regular folks like you and me are now getting in on investment opportunities that were once the exclusive domain of the ultra-rich.

Private Equity and Credit

Private equity has been outperforming public stocks, especially in more recent shaky, inflation riven economies.

Then there’s private credit, a haven for those seeking returns that don’t move in lockstep with the broader market.

The trend towards private credit makes sense. As traditional fixed-income options have become less and less attractive due to rising interest rates, investors are allocating more to private credit where returns can be stronger.

These small business financing notes, for example, offer accredited investors a 10% or 12% return whilst bringing some much sought after diversification to their portfolios.

Private credit has grown significantly over the last twenty years. Source Alts.co

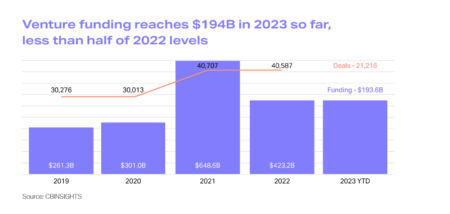

The Venture Capital Rebound

After a bit of a slump, venture capital is getting back on its feet, mirroring the recovery we’re seeing in public markets.

Quarter-over-quarter improvements in fundraising, deal volume, and valuations appear to be ahead, suggesting an upward shift in venture capital trends.

It doesn’t look like recovery will bring us anywhere near the record breaking figures of 2021 though.

Figures from 2023 VC activity. Source: Alluve.

Wrapping Up

2024 is shaping up to be a year where blending the old with the new in your investment strategy could lead to bigger gains and better protection against market madness.

If you’re looking to diversify your own portfolio or that of your clients, our partner Supervest provides two strong return, regular income alternative asset notes for accredited investors..